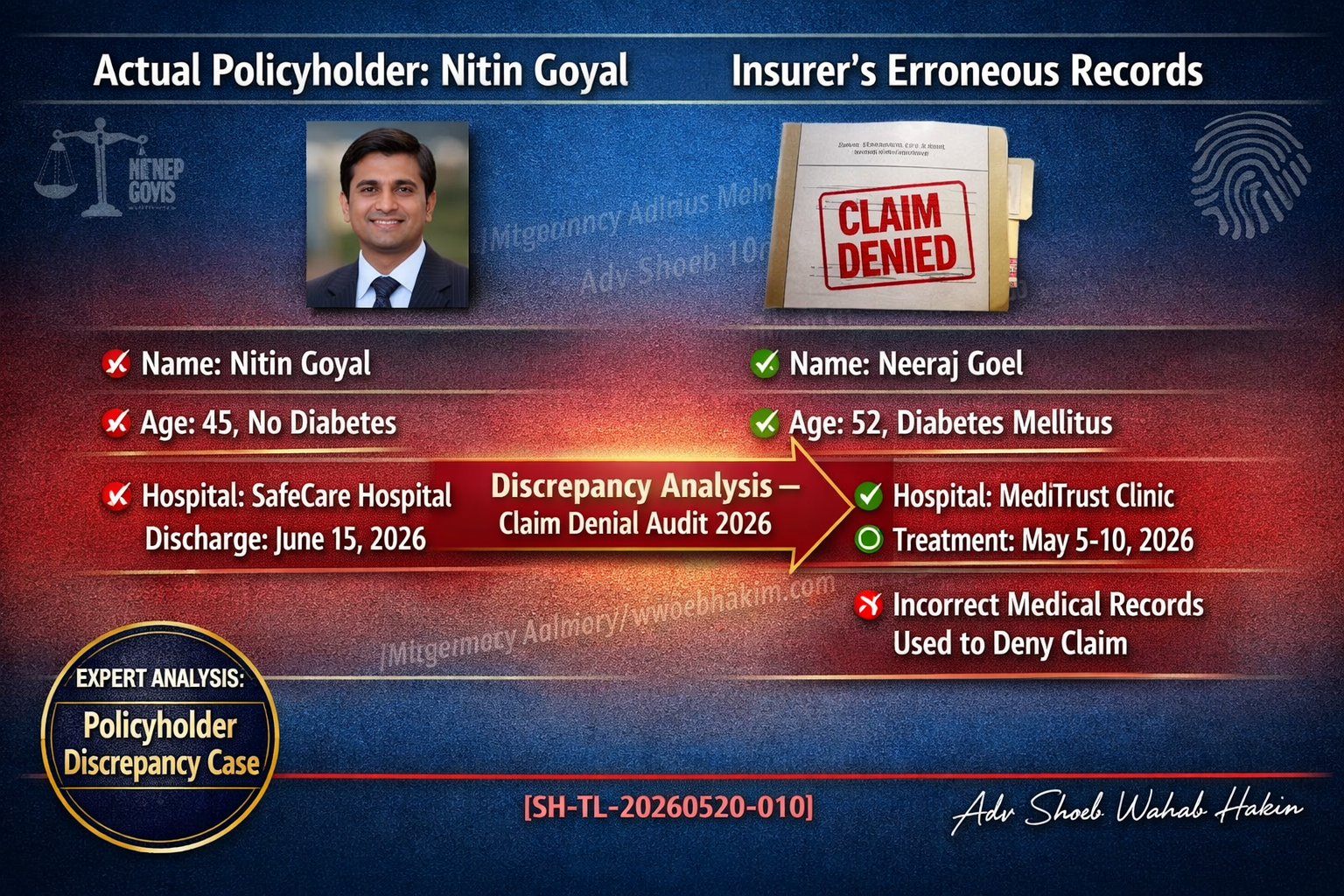

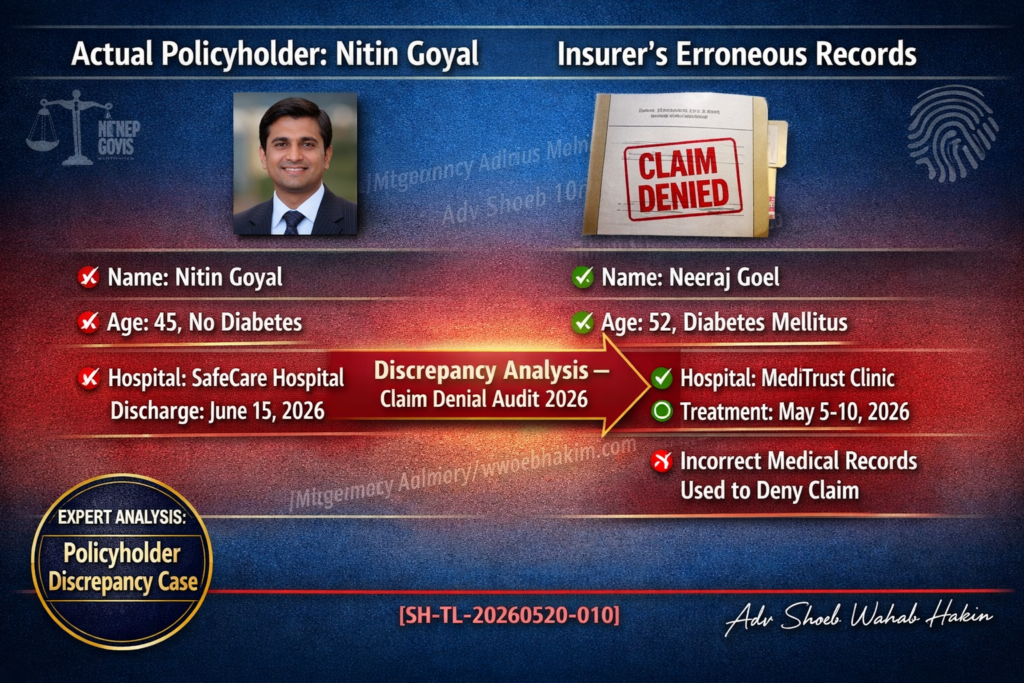

The insurer relied on another “Nitin Goyal’s” medical history – different address, different family, different wife’s name.

Introduction

Payal Goyal lost her husband in 2023. Then HDFC Life rejected a ₹1.29 crore insurance claim.

Nitin Goyal had taken multiple business loans from Axis Bank for M/s Krishna Steel Udyog, Jagadhri. Along with those loans, four insurance policies were issued under HDFC Life’s Group Credit Protect Plus Plan through the bank’s tie-up with the insurer.

Total insurance cover: ₹1,29,99,950. Premiums had already been collected.

The family believed that if anything unfortunate happened, the insurance would at least prevent financial collapse.

Then tragedy struck.

This article examines the case, the insurer’s defence, the Commission’s findings, and the final order.

The Facts

| Detail | Information |

|---|---|

| Policyholder | Nitin Goyal |

| Business | M/s Krishna Steel Udyog, Jagadhri |

| Loans from | Axis Bank |

| Insurance policies | Four policies under HDFC Life’s Group Credit Protect Plus Plan |

| Total cover | ₹1,29,99,950 |

| Date of death | 29 June 2023 |

| Hospital | Fortis Escorts Hospital, New Delhi |

| Cause of death | Sudden illness |

| Claim filed by | Payal Goyal (wife) |

The Repudiation

HDFC Life rejected the claim, alleging that Nitin Goyal had concealed a prior COVID-19 illness while taking the policies. The insurer accused him of suppression of material facts.

The legal basis for repudiation:

Under insurance law, the principle of uberrima fides (utmost good faith) requires policyholders to disclose all material facts. Nondisclosure can void the policy.

But here, the insurer’s evidence was flawed.

What the Consumer Commission Found

1. Insurer relied on records of another “Nitin Goyal”

During proceedings before the Consumer Commission, the insurer relied upon records allegedly connected to another “Nitin Goyal” to justify repudiation.

When evidence was examined carefully, the discrepancies became obvious:

- Different addresses

- Different family details

- One record even mentioned another wife’s name and different children

2. No authentic medical record

The Commission found that the insurer had failed to produce any authentic medical record proving that the deceased policyholder had suffered from COVID-19 before issuance of the policies.

3. Other insurers had settled claims

Other insurers including LIC, Max Life, Bajaj Allianz, and Star Health had already processed and settled claims relating to the same deceased person.

If there was material nondisclosure, why did other insurers pay?

The Commission’s Strong Observations

The Commission made strong observations against the insurer, noting:

“Insurance companies readily collect substantial premiums, but often scrutinise claims aggressively when the time comes to honour the promise.”

This observation reflects a judicial recognition of a widespread consumer grievance: insurers are quick to collect premiums but slow to pay claims.

The Final Order

| Direction | Amount |

|---|---|

| Claim amount | ₹1,29,99,950 |

| Interest | 7% annual from date of filing complaint |

| Compensation | As ordered |

| Litigation costs | As ordered |

The insurer was directed to pay the full claim amount with interest.

Why This Case Matters

1. Repudiation must be based on evidence, not assumption

The insurer assumed COVID-19 concealment. But they could not prove it. Worse, they relied on records of a different person.

2. Careless verification is not defence

Using another person’s records to deny a claim is not just a mistake. It is a failure of basic verification.

3. Other insurers’ conduct is relevant

When multiple insurers settle claims for the same deceased, a single insurer’s repudiation based on alleged nondisclosure becomes suspect.

4. Families already suffering should not be forced into litigation

The Commission recognised that when a family has already lost its earning member, forcing them into avoidable litigation through weak repudiation only deepens the hardship.

Legal Principles at Play

| Principle | Application |

|---|---|

| Utmost good faith (uberrima fides) | Insured must disclose material facts |

| Burden of proof on insurer | Insurer must prove nondisclosure was material and intentional |

| No repudiation without evidence | Cannot rely on incorrect records or assumptions |

| Consumer protection | Deficiency in service includes unfair claim repudiation |

Practical Takeaways for Policyholders

1. Document everything

Keep copies of all application forms, disclosures, and correspondence with the insurer.

2. Be truthful in disclosures

Non-disclosure of material facts is a valid ground for repudiation. Disclose all relevant medical history.

3. If claim is rejected, fight back

Do not accept repudiation without scrutiny. Approach the Consumer Commission. Many repudiations are overturned on appeal.

4. Note the timeline

The Commission awarded interest from the date of filing the complaint, not from the date of death. Early action matters.

Practical Takeaways for Insurers

1. Verify records before repudiation

Using another person’s records to deny a claim is unacceptable. Basic verification is mandatory.

2. Maintain authentic medical evidence

If you allege nondisclosure, you must prove it with authentic records – not assumptions or incorrect files.

3. Consistency matters

If other insurers have settled claims for the same deceased, your repudiation will face additional scrutiny.

4. Honour the promise

Premiums were collected. The insured passed away. The family suffered. Weak repudiation only adds to the hardship.

The Human Cost

Behind every insurance claim is a family.

Payal Goyal lost her husband. Then she had to fight for the insurance money that should have protected her financially.

The Commission recognised this. The order is not just about money. It is about holding insurers accountable.

Conclusion

Payal Goyal lost her husband in 2023. Then HDFC Life rejected a ₹1.29 crore insurance claim, alleging concealment of prior COVID-19 illness.

The Consumer Commission found that the insurer relied on records of another “Nitin Goyal” – different address, different family details, one record even mentioned another wife’s name and different children.

Other insurers including LIC, Max Life, Bajaj Allianz, and Star Health had already settled claims for the same deceased.

The Commission ordered HDFC Life to pay the full claim amount of ₹1,29,99,950 with 7% annual interest from the date of filing the complaint, plus compensation and litigation costs.

This case is a reminder: repudiation of insurance claims cannot be based on assumptions, careless verification, or unrelated records.

When a family has already lost its earning member, forcing them into avoidable litigation through weak repudiation only deepens the hardship.

Q: Can an insurer reject a life insurance claim based on similar names? Ans: No. HDFC Life Claim Rejection in this specific case proved that relying on unverified medical records of a namesake is a severe deficiency in service. Insurers must conclusively prove identity using specific identifiers like PAN or Aadhar.

Q: What is the principle of utmost good faith in insurance? Ans: Utmost good faith (uberrima fides) requires both parties to be completely honest. The policyholder must disclose all material medical facts, and the insurer must process claims fairly and accurately without using fabricated or unverified grounds for denial.

Q: Does the settlement of a claim by other insurers affect a pending dispute? Ans: Yes. The Consumer Commission heavily weighs industry consistency. If multiple major insurers (like LIC and Max Life) validate and settle a claim, a lone insurer’s repudiation based on alleged non-disclosure becomes highly suspect and difficult to defend in court.

What was the primary reason cited by HDFC Life for repudiating the claim?

- Ans: Alleged suppression of material facts regarding a prior COVID-19 illness.

What was the fatal flaw in the insurer’s documentary evidence?

- Ans: They relied on the medical records of a different person who shared the same name.

How much was the total insurance cover in dispute?

- Ans: ₹1,29,99,950.

True or False: Other insurers like LIC and Max Life had also rejected the claims for this individual.

- Ans: False; they had successfully settled the claims.

Adv. Shoeb Hakim

Insurance Law & Consumer Protection Advisor

📌 Follow me on LinkedIn for daily insurance and consumer law insights: https://www.linkedin.com/in/shoebhakim

📌 Visit my website for more articles: www.shoebhakim.com

♻️ Share this article with your network.

Disclaimer: This article is for informational purposes only and does not constitute legal advice.

Hashtags: #InsuranceClaim #HDFCLife #ConsumerCommission #InsuranceRepudiation #LifeInsurance #ClaimSettlement #ConsumerRights #InsuranceLaw #PayalGoyal #NitinGoyal #YamunaNagar #AxisBank #GroupCreditProtectPlus #COVID19 #SuppressionOfMaterialFacts #UtmostGoodFaith #UberrimaFides #DeficiencyInService #ConsumerProtection #InsuranceOmbudsman #ClaimRejection #WrongRecords #AnotherPerson #DifferentAddress #DifferentFamily #OtherInsurers #LICSettlement #MaxLife #BajajAllianz #StarHealth #InterestOnClaim #Compensation #LitigationCosts #FamilyHardship #EarningMember #ConsumerComplaint #DistrictConsumerCommission #InsuranceSector #IRDAI #InsuranceRegulation #PolicyholderRights #NomineeRights #SumAssured #GroupInsurance #CreditLinkedCover #LoanInsurance #BusinessLoan #MSME #SteelBusiness #Jagadhri #FortisEscortsHospital #SuddenIllness #AdvShoebHakim