One ₹100 payment. Ten steps. Four banks. One switch. One central bank. Seconds.

Introduction

₹18.41 trillion. That is not a budget. It is not a GDP figure. It is the volume of transactions UPI handles.

Behind every “payment successful” notification on your phone, there is a complex dance between payment apps, acquiring banks, issuing banks, the National Payments Corporation of India (NPCI), and the Reserve Bank of India (RBI).

This article breaks down the 10-step process that makes UPI the backbone of India’s digital economy.

The Scale of UPI

| Metric | Figure |

|---|---|

| Annual transaction volume | ₹18.41 trillion |

| Monthly transactions | Billions |

| Availability | 24/7/365 |

| Participating banks | Hundreds |

| Payment apps | Dozens |

| Users | Hundreds of millions |

UPI is not just a payment system. It is public infrastructure enabling private innovation.

The Key Players in a UPI Transaction

| Player | Role |

|---|---|

| Sender | Customer initiating payment |

| Receiver | Customer receiving payment |

| Payment App (PSP) | Interface (PhonePe, Google Pay, Paytm, etc.) |

| Acquiring Bank | PSP’s banking partner |

| Issuing Bank (Sender’s Bank) | Holds sender’s account |

| Issuing Bank (Receiver’s Bank) | Holds receiver’s account |

| NPCI | The switch – routes, validates, authorizes, settles |

| RBI | Final settlement authority |

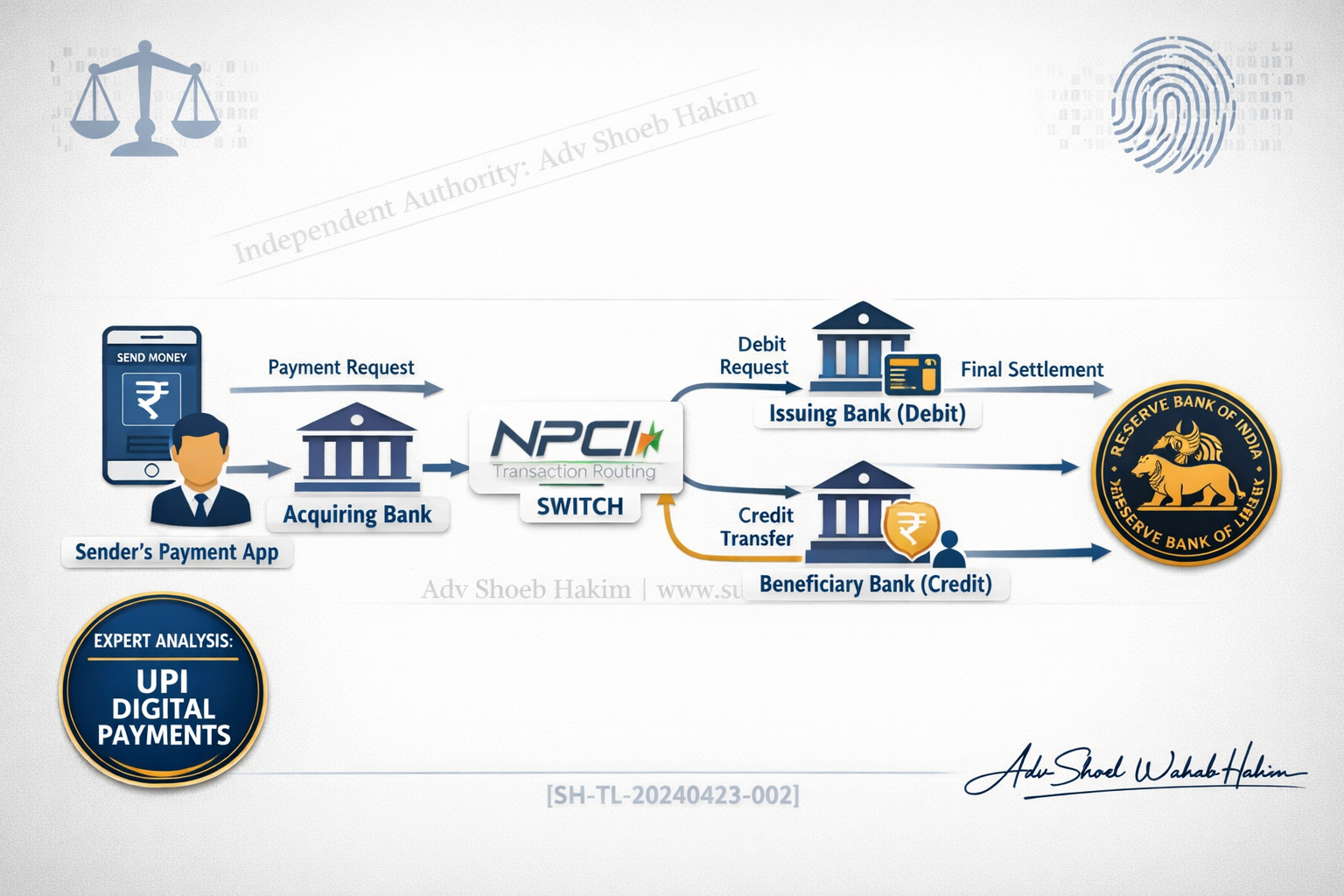

The 10-Step Journey of a ₹100 UPI Transaction

Step 1: User Initiates Payment

The sender opens a payment app, enters the receiver’s UPI ID and the amount, and authorizes the transaction with their UPI PIN.

Step 2: Payment App Encrypts and Forwards

The payment app encrypts the payment request and forwards it to its acquiring bank.

Step 3: Acquiring Bank to NPCI

The acquiring bank receives the request and forwards it to NPCI, the central switch that routes all UPI transactions.

Step 4: NPCI Validates Sender’s Account

NPCI validates the sender’s account details and fetches the receiver’s bank details from the UPI directory.

Step 5: NPCI Routes to Receiver’s Bank

NPCI routes the request to the receiver’s bank for validation.

Step 6: Receiver’s Bank Confirms, NPCI Authorizes Sender’s Bank

The receiver’s bank confirms that the UPI ID is valid. NPCI then authorizes the sender’s bank to debit the amount from the sender’s account.

Step 7: Sender’s Bank Debits and Confirms

The sender’s bank checks the balance, debits the amount, and sends a confirmation back to NPCI.

Step 8: NPCI Instructs Receiver’s Bank to Credit

NPCI instructs the receiver’s bank to credit the amount to the receiver’s account.

Step 9: Receiver’s Bank Credits and Notifies

The receiver’s bank credits the amount to the receiver’s account and notifies NPCI of successful credit.

Step 10: Final Settlement via RBI

NPCI ensures final settlement between the banks through the RBI’s settlement system.

All of this happens in seconds.

Visualizing the Flow

| Step | Actor | Action |

|---|---|---|

| 1 | Sender | Opens payment app, enters UPI ID, amount, PIN |

| 2 | Payment App | Encrypts request → acquiring bank |

| 3 | Acquiring Bank | Forwards request → NPCI |

| 4 | NPCI | Validates sender’s account, fetches receiver’s bank details |

| 5 | NPCI | Routes request → receiver’s bank |

| 6 | Receiver’s Bank | Confirms → NPCI authorizes sender’s bank to debit |

| 7 | Sender’s Bank | Debits amount → confirms to NPCI |

| 8 | NPCI | Instructs receiver’s bank to credit |

| 9 | Receiver’s Bank | Credits receiver → notifies NPCI |

| 10 | NPCI + RBI | Final settlement between banks |

Why UPI Works So Well

For Banks:

- Hold customer funds

- Process debit and credit instructions

- Settle through RBI

For Payment Apps (PSPs):

- Link bank accounts

- Provide user interface

- Innovate on customer experience

For NPCI:

- Operate the switch

- Ensure routing, security, and authorization

- Maintain uptime and scalability

For RBI:

- Oversee final settlement

- Regulate the ecosystem

- Ensure financial stability

The Result:

Interoperable, public infrastructure enabling private innovation.

What Makes UPI Different from Other Payment Systems

| Feature | UPI | Traditional Cards | Bank Transfer |

|---|---|---|---|

| Requires IFSC code | No | N/A | Yes |

| Requires card number | No | Yes | No |

| 24/7 availability | Yes | Yes | Limited |

| Interoperable across apps | Yes | Limited | Limited |

| Virtual payment address | Yes | No | No |

| Settlement speed | Seconds | Seconds | Hours/days |

The Role of NPCI: The Invisible Switch

NPCI is the most important player in the UPI ecosystem that most users have never heard of.

NPCI’s Responsibilities:

- Routing transactions between banks

- Validating UPI IDs

- Authorizing debits and credits

- Ensuring security and encryption

- Settling funds between banks

- Maintaining 24/7 uptime

Without NPCI, UPI would not exist.

The Role of RBI: Final Settlement Authority

While NPCI handles the routing and authorization, RBI handles final settlement.

How Settlement Works:

- Throughout the day, banks owe each other money from UPI transactions

- NPCI nets these obligations

- At the end of the day, banks settle the net amount through RBI

- RBI ensures that the settlement is final and irrevocable

Why the User Experience Is Simple

The complexity is hidden from the user.

What the user sees:

- Enter UPI ID

- Enter amount

- Enter PIN

- “Payment successful”

What happens behind the scenes:

- 10 steps

- Multiple banks

- Encryption

- Validation

- Routing

- Authorization

- Debit

- Credit

- Settlement

The simplicity for the user is the result of extreme complexity behind the scenes.

The Future of UPI

Potential developments:

- International expansion: UPI already works in several countries. More to come.

- Credit on UPI: Credit lines linked to UPI IDs (already piloted)

- Offline UPI: Transactions without internet connectivity

- AI-powered fraud detection: Real-time risk scoring

- Higher transaction limits: As trust and infrastructure mature

Conclusion

UPI is not just a payment system. It is public infrastructure enabling private innovation.

One ₹100 transaction involves payment apps, acquiring banks, NPCI, sender’s bank, receiver’s bank, and RBI. Encryption, validation, routing, authorization, debit, credit, settlement. All in seconds.

The user sees “payment successful.” Behind the scenes, a 10-step dance happens across India’s financial infrastructure.

That is the magic of UPI.

Adv. Shoeb Hakim

Digital Payments & Fintech Advisor

📌 Follow me on LinkedIn for daily fintech and digital payment insights: https://www.linkedin.com/in/shoebhakim

📌 Visit my website for more articles: www.shoebhakim.com

♻️ Share this article with your network.

Disclaimer: This article is for informational purposes only and does not constitute legal advice.

Hashtags: #UPI #NPCI #DigitalPayments #Fintech #RBI #IndiaStack #DigitalIndia #BHIM #PhonePe #GooglePay #Paytm #AmazonPay #PaymentSystems #Banking #FinancialInfrastructure #Interoperability #PublicInfrastructure #PrivateInnovation #RealTimePayments #ImmediateSettlement #PaymentGateway #AcquiringBank #IssuingBank #Settlement #RuPay #AadhaarPay #CreditOnUPI #OfflineUPI #InternationalUPI #AdvShoebHakim

#DigitalPublicInfrastructure #RealTimePayments #PaymentSwitch #FinancialInclusion #FintechStrategy #UPI2026 #TechGovernance #DigitalIndia