Effective 1 April 2026, CAs and CA firms gain greater flexibility to showcase their expertise professionally and ethically.

Introduction

For decades, Chartered Accountants built their reputation through relationships and referrals. That worked. But the world changed. Technology. Digital presence. Specialised services. International competition.

The ICAI Code of Ethics has now changed too.

Effective 1 April 2026, the revised ICAI Code of Ethics gives Chartered Accountants and CA firms greater flexibility to showcase their expertise, capabilities, and services in a professional and ethical way.

This article analyzes the key changes, what remains unchanged, and the opportunities ahead.

Why the Change Was Needed

| Technology | New tools, new ways of working |

| Digital presence | Clients expect online visibility |

| Specialised services | Forensic accounting, AI, sustainability consulting |

| International competition | Indian CAs compete globally |

| Client expectations | Faster, more accessible, transparent |

The profession needed to adapt while maintaining its core values.

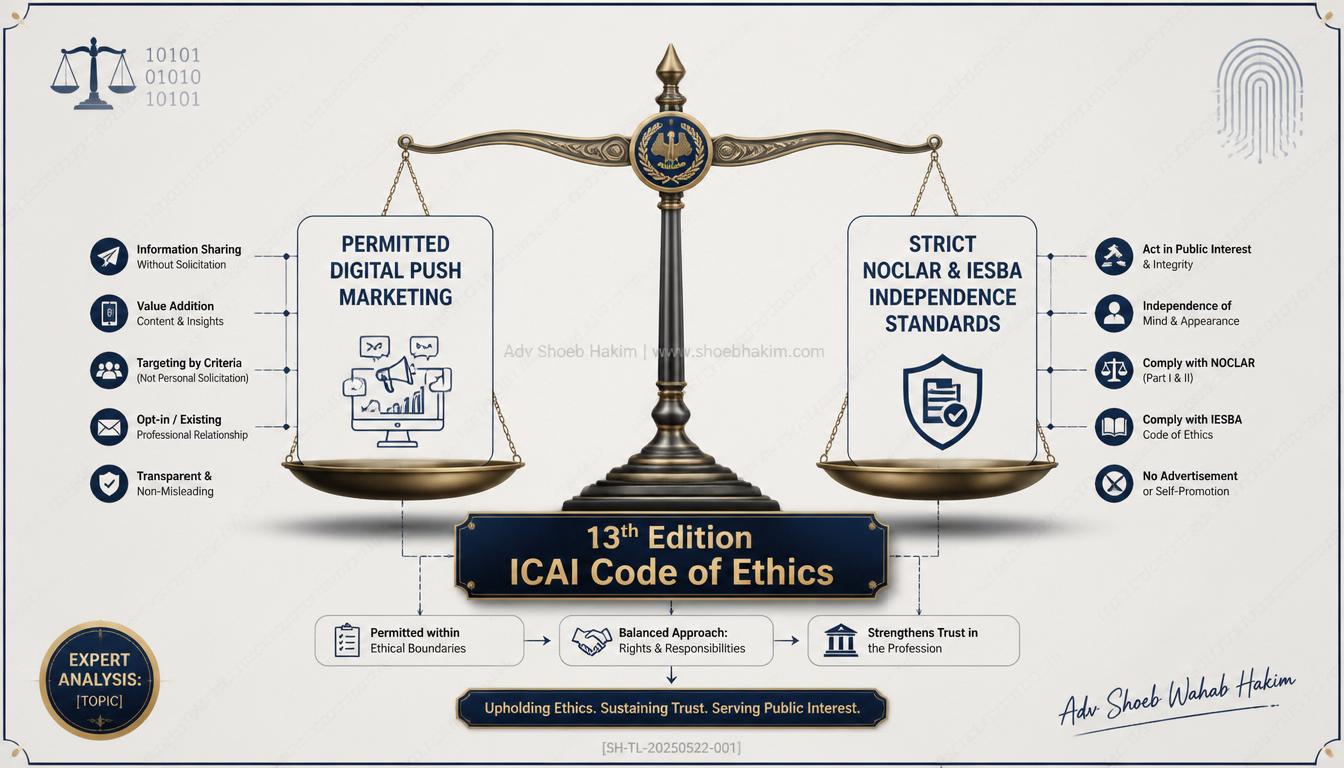

What Has Changed

The revised Code of Ethics introduces:

| Change | Description |

|---|---|

| Professional visibility | CAs and CA firms can showcase expertise more flexibly |

| Online presence | Updated rules for digital and online promotion |

| Non-exclusive services | Ethical promotion of non-exclusive services permitted |

| Emerging fields | Opportunities in AI, forensic accounting, sustainability, research services |

| Global alignment | Indian standards closer to global ethical benchmarks |

What Remains Unchanged

The core principles of the profession stay unchanged:

- Integrity – Being straightforward and honest

- Objectivity – Not allowing bias or conflict of interest

- Professional competence – Maintaining knowledge and skill

- Ethical behaviour – Complying with the law and avoiding discreditable conduct

Trust and professionalism remain the foundation.

Opportunities for the Profession

For individual CAs:

- Build a professional online presence

- Showcase specialised expertise (forensic accounting, AI, sustainability)

- Reach clients beyond traditional referral networks

For CA firms:

- Promote non-exclusive services ethically

- Compete internationally with updated standards

- Attract younger clients through digital visibility

For new and smaller firms:

- Level the playing field with larger firms

- Build reputation through demonstrated expertise, not just history

- Specialise in emerging fields without restrictive barriers

Comparison with Global Standards

| Jurisdiction | Ethical Framework | Promotion Rules |

|---|---|---|

| India (ICAI) | Code of Ethics (revised 2026) | Updated for digital age |

| UK (ICAEW) | Code of Ethics (IESBA-based) | Restricted but evolving |

| US (AICPA) | Code of Professional Conduct | More permissive |

| Global (IESBA) | International Code of Ethics | Benchmark for all |

India is now closer to global ethical benchmarks while maintaining its distinct professional identity.

The Role of ICAI Leadership

The reforms were led by the ICAI leadership and the Ethical Standards Board. Their recognition of the profession’s need for adaptability is commendable.

Key acknowledgements:

- Relationships and referrals remain vital

- Technology and digital presence demand adaptability

- International competition requires flexibility

- Core values must stay unchanged

The True Opportunity

The true opportunity now lies in using this flexibility wisely, with an unwavering focus on:

- Knowledge – Deepening expertise

- Quality – Maintaining high standards

- Credibility – Building and preserving trust

- Client value – Delivering meaningful outcomes

Improved visibility is a tool. What matters is how you use it.

Conclusion

For decades, the profession has built its reputation through relationships and referrals. While these remain vital, today’s environment demands greater adaptability, driven by technology, digital presence, specialised services, and international competition.

The reforms acknowledge this shift by:

- Updating professional visibility and online presence

- Enabling ethical promotion of non-exclusive services

- Creating opportunities in emerging fields such as AI, forensic accounting, sustainability, and research services

- Bringing Indian standards closer to global ethical benchmarks

Importantly, the core principles of the profession—integrity, objectivity, professional competence, and ethical behaviour—stay unchanged. These reforms enhance visibility while maintaining the trust and professionalism that define the profession.

The future of the profession will be shaped not just by improved visibility but by how effectively we blend innovation with the enduring values that have consistently earned public trust.

Q: What marketing activities are now permitted for CA firms under the 2026 ICAI guidelines?

Ans: Under the ICAI Code of Ethics Revised guidelines, CA firms can maintain professional websites, utilize social media for educational content, and use “push technology” (like targeted newsletters) to ethically promote non-exclusive advisory and consulting services. However, all content must remain strictly factual and objective.

Q: Can a Chartered Accountant publish client testimonials on their firm’s website?

Ans: No. Despite the liberalization of digital visibility, publishing client testimonials, words of appreciation, or displaying specific client logos remains strictly prohibited, as it violates the core principles of objective and non-laudatory professional communication.

Q: How do the new rules affect auditor independence regarding Public Interest Entities (PIEs)?

Ans: The 2026 Code strictly enforces auditor independence by adopting the 2024 IESBA standards. An audit firm is explicitly prohibited from accepting the statutory audit of a Public Interest Entity if it has previously provided a non-assurance service that creates a self-review threat to the financial statements.

When does the revised 13th Edition of the ICAI Code of Ethics officially come into effect?

- Ans: April 1, 2026.

Under the new guidelines, can a CA firm use “push technology” to promote its statutory audit services?

- Ans: No, push technology is only permitted for non-exclusive services, such as consultancy and advisory work.

The new ICAI Code of Ethics is converged with the 2024 edition of which global standard?

- Ans: The International Ethics Standards Board for Accountants (IESBA) Code of Ethics.

What does the expanded NOCLAR provision require auditors of listed entities to do?

- Ans: It requires them to proactively address and report potential non-compliance with laws and regulations encountered during an audit engagement.

Adv. Shoeb Hakim

Professional Ethics & Corporate Governance Advisor

📌 Follow me on LinkedIn for daily professional ethics and corporate governance insights: https://www.linkedin.com/in/shoebhakim

📌 Visit my website for more articles: https://www.shoebhakim.com

📌 Visit my website for legal knowledge: https://www.vakilverse.com

📌 Visit my website for research fellowship: https://www.legalcomplaince.in

♻️ Share this article with your network.

Disclaimer: This article is for informational purposes only and does not constitute legal advice.

Hashtags: #AdvShoebHakim #ICAI #CodeOfEthics #CharteredAccountant #CAProfession #Ethics #ProfessionalStandards #ICAIReforms #CAFirms #ForensicAccounting #Sustainability #AI #ResearchServices #ProfessionalVisibility #OnlinePresence #NonExclusiveServices #GlobalBenchmarks #IESBA #ICAEW #AICPA #Integrity #Objectivity #ProfessionalCompetence #EthicalBehaviour #TrustAndProfessionalism #EthicalStandardsBoard #ICAILeadership #NewerFirms #SpecialisedPractices #EmergingFields #DigitalAge #InternationalCompetition #ClientValue #KnowledgeQualityCredibility #ProfessionalDevelopment #CACommunity #IndiaCA #GlobalCA #AccountingProfession #AuditProfession #TaxProfession #ConsultingProfession #AdvisoryServices #FinancialReporting #Compliance #RiskManagement #Governance #CorporateGovernance #ProfessionalServices #BusinessAdvisory #FinancialConsulting #StrategicAdvisory #DigitalTransformation