Empowering banks, but procedure-driven. Non-compliance can invalidate entire recovery proceedings.

Introduction

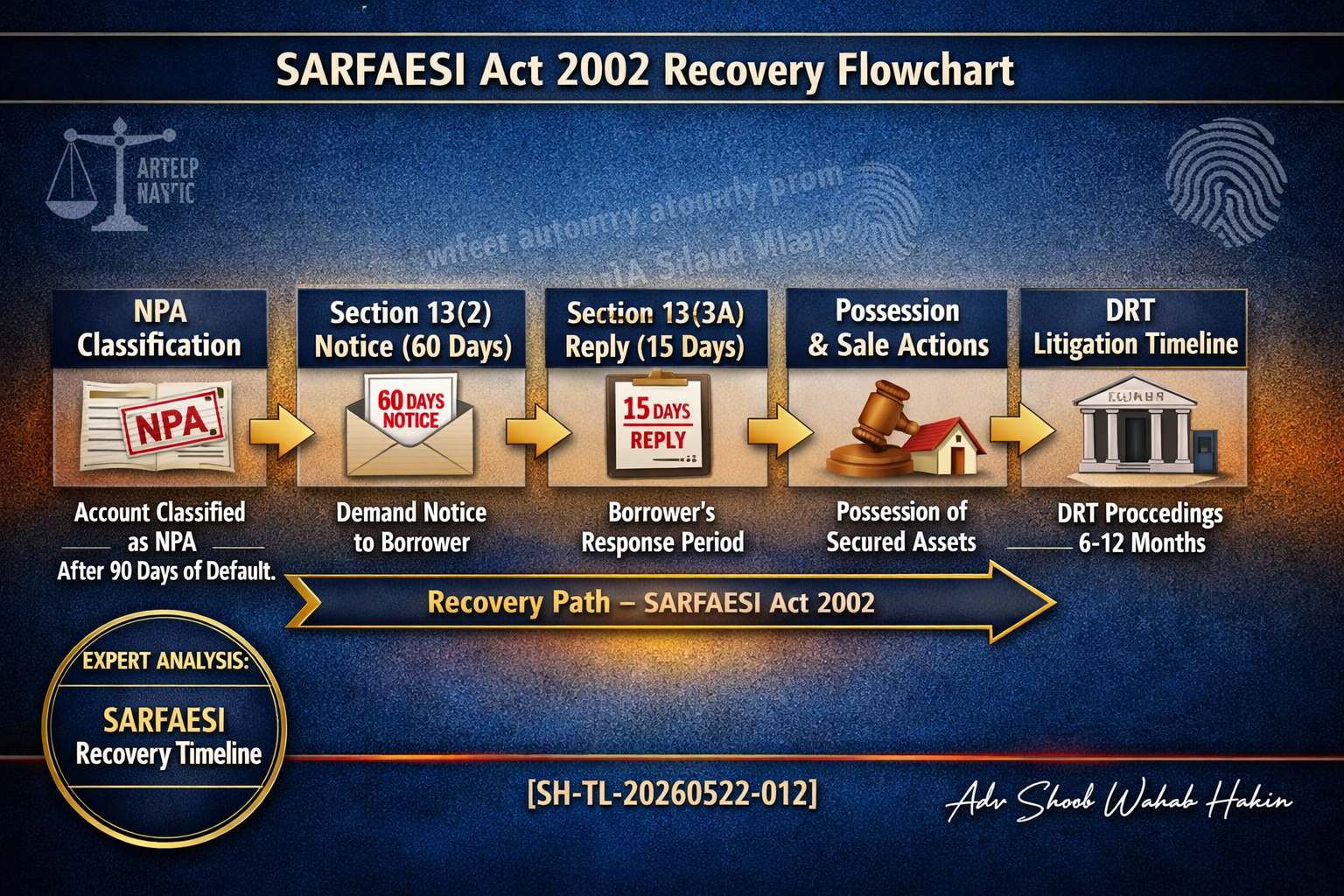

The SARFAESI Act, 2002 was enacted to empower banks and financial institutions to enforce security interests and recover debts without court intervention, creating a faster mechanism for tackling Non-Performing Assets (NPAs).

However, the exercise of these powers is heavily procedure-driven. Even minor non-compliance with statutory requirements can invalidate recovery proceedings.

Power without compliance is a trap. One missed deadline. One defective notice. One procedural error. And the bank starts from zero.

This article provides a comprehensive guide to SARFAESI compliance, litigation timelines, strategic considerations, and defences.

Key Compliance Requirements Under SARFAESI

| Requirement | Details |

|---|---|

| NPA classification | Loan account must first be classified as an NPA under RBI norms |

| Demand notice | Mandatory 60-day notice under Section 13(2) |

| Borrower objections | Must be replied to within 15 days under Section 13(3A) |

| Possession measures | Under Section 13(4) only after statutory compliance |

| Valuation & auction notice | Mandatory valuation, reserve price fixation & 30-day auction notice |

| CERSAI registration | Within 30 days – essential for enforcement rights |

Why compliance matters:

Courts have repeatedly held that non-compliance at any stage can invalidate the entire recovery proceeding. Banks must follow every step in the correct sequence.

Important Litigation & Appeal Timelines

| Action | Timeline |

|---|---|

| Securitisation Application (SA) before DRT | Within 45 days |

| Appeal before DRAT | Within 30 days |

Pre-deposit requirement:

- 50% of debt amount

- Reducible to 25% at Tribunal discretion

Practical tip: Delay beyond these timelines results in dismissal. Extensions are rarely granted.

e-DRT & Filing Requirements

What has changed:

- e-filing through the e-DRT portal is now mandatory

- Physical paper books must also be filed within 7 working days

- Pleadings must comply with prescribed formatting standards

Common filing errors:

- Incomplete documents

- Missing affidavits

- Improper formatting

- Late physical filing after e-filing

Result of non-compliance: DRT may reject the application or refuse to entertain it on technical grounds.

Strategic Considerations for Banks

| Strategy | Purpose |

|---|---|

| Lodge Caveat Petitions | Avoid ex-parte stay orders |

| Simultaneous proceedings | Pursue DRT and SARFAESI remedies together |

| Interim protections | Seek attachment orders or appointment of receivers |

Why caveat petitions matter:

If a borrower files a case without notice to the bank, the bank may not have an opportunity to be heard before an interim stay is granted. A caveat petition prevents this.

Simultaneous proceedings:

Banks can pursue DRT proceedings (recovery certificate) and SARFAESI proceedings (possession and sale) simultaneously. They are not mutually exclusive.

Strategic Defences for Borrowers

| Defence | Application |

|---|---|

| Challenge defective notices | Demand notice, possession notice, auction notice |

| Section 13(3A) violation | Bank ignored borrower objections |

| Agricultural land exemption | Statutory exemption for protected land |

| Right of redemption | Available before sale certificate is issued |

Timing matters: Right of redemption exists until the sale certificate is issued. Once issued, the borrower’s rights are extinguished.

Grounds for Challenging Recovery Action

| Ground | Explanation |

|---|---|

| Invalid NPA classification | Account was not actually an NPA under RBI norms |

| No reasoned reply within 15 days | Bank violated Section 13(3A) |

| Incorrect debt quantification | Bank demanded more than actually due |

| Defective possession or auction notices | Notice not properly served or not as prescribed |

| Violation of mandatory procedures | Any step not followed as per statute |

Key principle: Courts take procedural compliance seriously. Even a technical violation can invalidate the entire recovery.

Essential Documents for Securitisation Application (SA)

| Document Type | Examples |

|---|---|

| Loan agreements | Loan documents, mortgage records |

| NPA certificate | NPA classification certificate |

| Financial records | Statement of account |

| Notices | Demand notice, possession notice |

| Service proof | Delivery confirmation, publication records |

| Correspondence | Borrower representations, bank replies |

| Procedural documents | Affidavits, IA applications, Vakalatnama |

Missing documents = missing case. Ensure complete documentation before filing.

Regulatory Penalties

| Violation | Penalty |

|---|---|

| Failure to register with CERSAI | May attract daily penalties |

| Non-compliance with RBI directions | Substantial fines for ARCs |

| Serious contraventions | Imprisonment, fines, or both |

For banks and ARCs: Compliance is not optional. Regulators are watching.

Conclusion

The SARFAESI Act, 2002 is a powerful tool for debt recovery. But power without compliance is a trap.

Every requirement matters: NPA classification, 60-day demand notice, reply to objections within 15 days, proper possession measures, valuation, auction notice, CERSAI registration.

Every timeline matters: 45 days for DRT, 30 days for DRAT, 50% pre-deposit (reducible to 25%).

Every strategic decision matters: caveat petitions, simultaneous proceedings, interim protections.

For banks, compliance is the difference between recovery and liability. For borrowers, procedural challenges are the difference between losing property and protecting it.

Q: Can a bank take possession of my property without a court order under SARFAESI? Ans: Yes. The SARFAESI Act 2002 Recovery mechanism allows banks to take possession of secured assets without court intervention, provided the account is classified as an NPA and the mandatory 60-day notice under Section 13(2) has expired without resolution.

Q: What is a Caveat Petition and why do banks use it? Ans: A Caveat Petition is a legal notice filed by the bank at the DRT. It ensures that if a borrower tries to file a case to stop the recovery process, the Tribunal will not grant an emergency “ex-parte” stay without first hearing the bank’s side of the story.

Q: Can agricultural land be seized under the SARFAESI Act? Ans: No. Section 31(i) of the SARFAESI Act provides a statutory exemption for agricultural land, protecting it from being seized or auctioned under this specific recovery mechanism.

Under Section 13(2), how many days must the demand notice provide to the borrower?

- Ans: 60 days.

What is the mandatory timeframe for a bank to reply to a borrower’s objections under Section 13(3A)?

- Ans: 15 days.

How many days does a borrower have to file a Securitisation Application (SA) before the DRT?

- Ans: 45 days.

True or False: A borrower’s right of redemption continues indefinitely after the property is auctioned.

- Ans: False; it extinguishes once the sale certificate is issued.

Adv. Shoeb Hakim

Banking & SARFAESI Advisor

📌 Follow me on LinkedIn for daily banking and debt recovery insights: https://www.linkedin.com/in/shoebhakim

📌 Visit my website for more articles: www.shoebhakim.com

♻️ Share this article with your network.

Disclaimer: This article is for informational purposes only and does not constitute legal advice.

Hashtags: #SARFAESI #BankingLaw #NPA #DebtRecovery #DRT #DRAT #CERSAI #RBI #FinancialLaw #BankingCompliance #AssetRecovery #Securitisation #SARFAESIAct #BankingRegulation #SecuredCreditor #EnforcementOfSecurityInterest #NPARecovery #BankLitigation #DebtEnforcement #FinancialRecovery #BankingLawyer #SARFAESICounsel #NCLT #IBC #Insolvency #CreditRecovery #BankingSector #CommercialLaw #LegalStrategy #ComplianceMatters #DueDiligence #LenderRights #BorrowerRights #CERSAICompliance #SARFAESITimelines #DRTProceedings #DRATAppeal #PreDeposit #SecuritisationApplication #Efiling #CaveatPetition #RightOfRedemption #AgriculturalLandExemption #PossessionNotice #AuctionNotice #LoanRecovery #EnforcementRemedies #AttachmentOrder #ReceiverAppointment #AdvShoebHakim